How to Choose Between FHA vs. Conventional Loans

Posted: September 04, 2025

At McCaffrey Home Mortgage, we believe that choosing the right mortgage is as important as choosing the right home. With so many loan programs available today, it can be difficult to know where to begin. That's where our team of experts comes in. We'll provide you with a basic understanding of the different loan options available and help you understand key differences so you can select the loan that's best for you.

Two of the most common loan options for first-time buyers are Conventional Loans and FHA Loans. While both help you achieve the same goal (homeownership), they work very differently.

Let’s break them down so you can decide which might be the best fit for you.

What is a Conventional Loan?

A conventional loan is not backed by the government. Instead, it comes from private lenders like banks, credit unions, or mortgage companies.

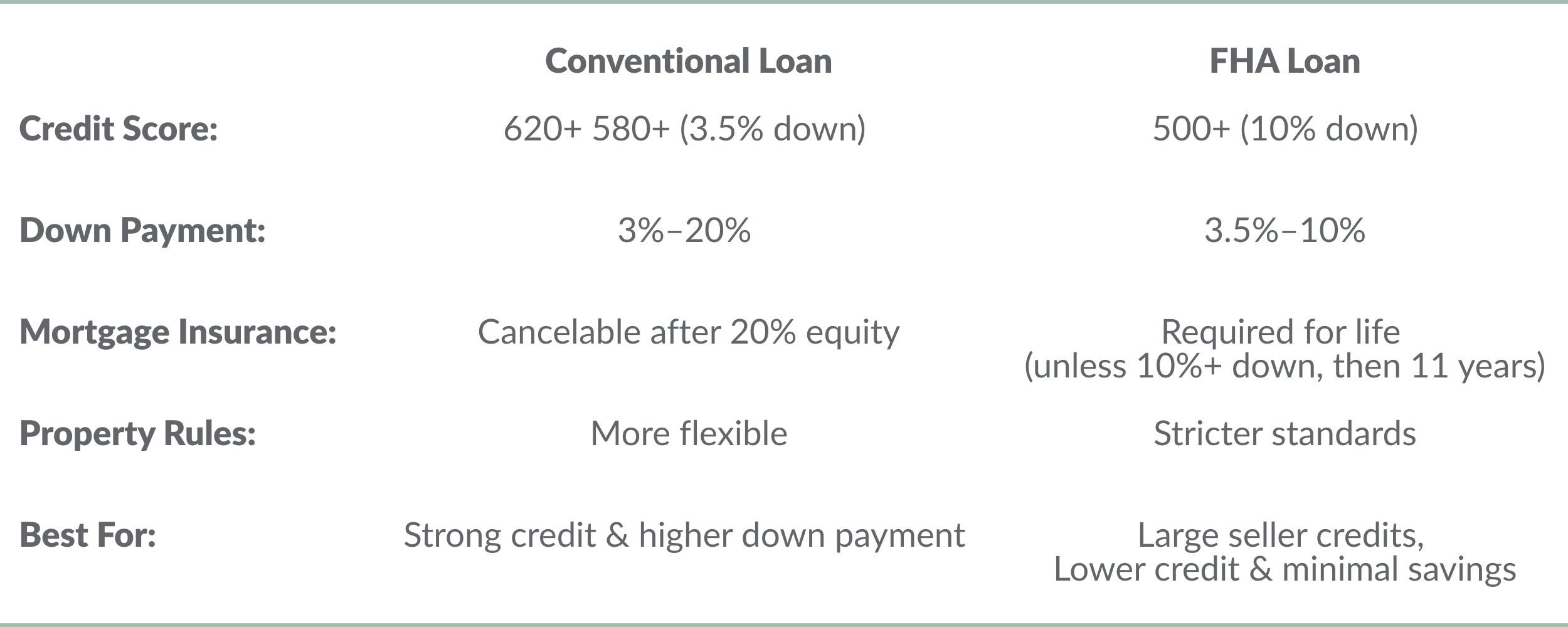

- Credit Score Requirements: Typically, 620 or higher.

- Down Payment: As low as 3% with some programs, but putting 20% down helps you avoid PMI (private mortgage insurance).

- Mortgage Insurance: If you put less than 20% down, PMI is required, but it can be canceled once you reach 20% equity.

- Max Seller Credit: up to 3% with less than 10% down, up to 6% with 10%-25% and up to 9% with 25% or more down

- Best For: Buyers with good credit, steady income, and some savings for a down payment.

What is an FHA Loan?

An FHA loan is backed by the Federal Housing Administration. This makes it more accessible for buyers with lower credit or smaller savings.

- Credit Score Requirements: As low as 580 with 3.5% down, or 500 with 10% down.

- Down Payment: Minimum of 3.5%.

- Mortgage Insurance (MIP): Includes both an upfront fee (1.75% of the loan) and annual premiums. For most buyers, MIP lasts the life of the loan.

- Max Seller Credit: up to 6% with the minimum down

- Best For: Buyers with large incentive from a seller and minimum down payment, lower credit scores or higher debt amount who still want to purchase a home.

Key Differences

Which Loan is Right for You?

- If you have good credit and at least 10–20% for a down payment, a conventional loan may save you money in the long run since you can get rid of PMI.

- If you have a lower credit score or limited funds, an FHA loan is often easier to qualify for and could be your ticket into homeownership.

Why Choose McCaffrey Home Mortgage?

At McCaffrey, we not only want you to feel confident in your home buying decision but also well-equipped for the journey ahead. We understand there are many choices available when it comes to selecting a home mortgage lender, and we are confident that our team of experts stands out from the rest. Learn more about Finance | McCaffrey Homes, speak with a member of our McCaffrey mortgage team today!